Find out how much you can borrow - call us today!

Fermanagh Mortgages

About Me:

I have worked in the Financial Services Industry in many roles, over the past 35 years.

I am a motivated, driven adviser and at each stage of the process, I will always work hard my clients.

- Our extensive knowledge means we will guide clients to find a mortgage rate to suit their needs

- We have access to 'whole of market' mortgage rates and deals with all mainstream lenders

- We do the hard work for the client to 'make it happen'!

- We have strong knowledge of all property scenarios and client circumstances

We have not advertised our services for near 20 Years, as our new clients are ALL from existing client referrals.

Life Outside Work:

Outside work I am involved in my local community, and support several local charities.

As a dedicated gardener, I spend much of spare time in the garden tending to my vegetable patch, and find the process of growing my own food and working in the wider garden relaxing and very satisfying.

I have a keen interest in property investment and do regularly support my sons with the maintenance & DIY tasks within their properties. I also enjoy travelling and try, each year, to visit at least one new country.

Why Fermanagh Mortgages Exist:

We are a local Brokerage with strong local knowledge. Being a 'whole of market' Broker, we can always provide you with an extensive research approach, to show all of the lenders that may meet your needs:

- CLIENT FIRST: With a personal service and attention to detail

- WIDE CHOICE: Our recommendation is never tied to any one lender; we are 'whole of market'

- AT TIME TO SUIT YOU: Appointments to suit you - we operate day and evening appointments

- EXPERT KNOWLEDGE: We have strong connections with local Solicitors & Estate Agents etc.

Being a local, NI based Broker, we can therefore deal with all types of Mortgages and Protection planning etc.

Our Services

Your Next Property Move:

Protect The Things That Matter:

Your Next Property Move:

Purchasing a property to live in is one of the biggest decisions a person might ever make!

Mortgages can often be seen as complex!

We will guide you through this whole process.

WE CAN ANSWER

How much can you borrow on Mortgage?

How much Deposit do I need to put down?

Can I have someone else on the mortgage?

How much will the mortgage cost me

Purchasing a property to live in is one of the biggest decisions a person might ever make!

Mortgages can often be seen as complex!

We will guide you through this whole process.

WE CAN ANSWER

How much can you borrow on Mortgage?

How much Deposit do I need to put down?

Can I have someone else on the mortgage?

How much will the mortgage cost me each month?

We deal with everything, from the initial enquiry, through to the Mortgage Completion.

Buy to Let Mortgages:

Protect The Things That Matter:

Your Next Property Move:

With the high demand for rental properties, we see so much growth in buy to let mortgages.

Often its existing landlords who are buying additional properties, while others are investing into property for the very first time!

WE CAN HELP:

This is an area that we have access to many specialist lenders, offering a range of rates, with mortgage

With the high demand for rental properties, we see so much growth in buy to let mortgages.

Often its existing landlords who are buying additional properties, while others are investing into property for the very first time!

WE CAN HELP:

This is an area that we have access to many specialist lenders, offering a range of rates, with mortgage terms long in your 90's!

'Buy to Let' Mortgage split into two options:

* Personal 'Buy to Let' Mortgages

* Limited Co 'Buy to Let' Mortgages

*****

Age in only a number when it comes to 'Buy To Let' mortgages! (you are rarely ever too old!)

Protect The Things That Matter:

Protect The Things That Matter:

Protect The Things That Matter:

When times are good we can all buy the things we work hard to afford.

At Fermanagh Mortgages we will also review your circumstances to ensure you have the right protection in place to deal with the 'what if's':

When times are good we can all buy the things we work hard to afford.

At Fermanagh Mortgages we will also review your circumstances to ensure you have the right protection in place to deal with the 'what if's':

With mortgages/Loans/Credit Cards and other debt, come the responsibility to make the monthly repayment regardless of your health!

****

We can arrange all type of personal protection:

Income Protection - to replace your salary

Mortgage Protection - Life Cover/Serious Illness

Family Protection - to provide for loved ones

Private Medical Insurance

Buildings & Contents Insurance

What is a 'Decision in Principle' (DIP)?

A Decision in Principle (DIP) also known as an Agreement in Principle (AIP) & Mortgage in Principle:

It is a non-binding, written statement from a lender confirming how much they may be willing to lend you based on initial financial checks. We use this process to start your mortgage journey, and generate a 'DIP Certificate' which you can use with the Estate Agents when seeking to make an offer.

- It is a guide to the amount of mortgage a lender may offer you

- Most Estate Agents will ask to see this proof

- Often required to even place an bid on a property (Known as 'proof of funds')

- Your 'DIP' shows sellers you are a serious potential purchaser

- Usually valid for 30-90 days (varies between lenders)

WHY IS THIS USEFUL?

- Proof of Funds: It indicates to other relevant parties, that you can secure a mortgage

- Budgeting: It helps you understand your max. borrowing limit & the expected monthly costs

- Speed: It can accelerate the application process when you find a property

Type of Mortgage Interest Rates:

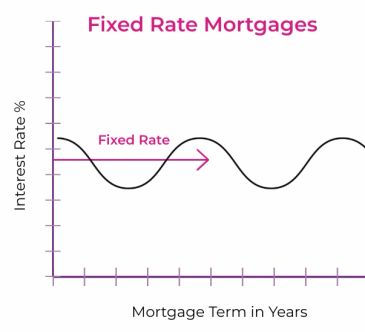

Fixed Rate Mortgage

Discounted Mortgage Rate

Fixed Rate Mortgage

Typically, a fixed rate can be anything from 1 year to 10 years

Many home owners prefer a fixed rate, so that they have the peace of mind of a fixed payment!

Regardless of what the mortgage rates do, your payment is FIXED until the end of the fix period.

***

The majority of 'First Time Buyers' or those working on a tight budget would usually be encouraged to consider this type of rate!

Tracker Mortgage

Discounted Mortgage Rate

Fixed Rate Mortgage

A Tracker Mortgage usually 'tracks' the Bank of England Base rate - by a set % margin

This type of Mortgage rate will change over the years, as interest 'Base Rate' change.

Typically, this is considered more by experienced borrowers OR those with enough disposable income, to still afford their mortgage, even if their payments went up subst

A Tracker Mortgage usually 'tracks' the Bank of England Base rate - by a set % margin

This type of Mortgage rate will change over the years, as interest 'Base Rate' change.

Typically, this is considered more by experienced borrowers OR those with enough disposable income, to still afford their mortgage, even if their payments went up substantially in the future!

***

In times of rising interest rates, a mortgage holder can quickly see their payments increase, hence this is often considered a more risky option.

Discounted Mortgage Rate

Discounted Mortgage Rate

Discounted Mortgage Rate

This is a variable rate, which is linked to the lender's full 'Standard Variable Rate'.

With this rate your monthly payment can also change. Your payment could go up OR down depending on the lenders 'SVR' changes.

***

Often considered more as an option by those with smaller mortgages OR those who have sufficient disposable income to meet eve

This is a variable rate, which is linked to the lender's full 'Standard Variable Rate'.

With this rate your monthly payment can also change. Your payment could go up OR down depending on the lenders 'SVR' changes.

***

Often considered more as an option by those with smaller mortgages OR those who have sufficient disposable income to meet even a much higher mortgage payment should their payment have drastically increased!

(This is the typical rate many go onto when their deal ends - hence, we encourage all to seek advice when you rate is near an end!)

Home Insurance

Why take Home Insurance through a Broker like us?

Alongside your mortgage, all lenders will insist that you have Building Insurance in place to protect your home from all of the typical risks, such as storm damage/fire/flood/Escape of water etc:

For owner occupiers, we recommend Home Insurance, which combines Buildings & Contents Insurance.

- Our aim is to keep your home protected no matter what happens (Outside your control)

- We normally recommend cover for buildings, contents and goods away from home.

- By reviewing annually you eliminate the risks of under insurance

- If we arrange your policy we are also here to support you with a claim

- You home is your biggest asset - therefore its important that the insurance is correctly arranged!

We have access to a wide range Home Insurance providers, and we work with you to bring the best, tailored cover to suit!

Extras you can consider adding:

Home Insurance can also include many additional benefits which offer additional peace of mind.:

Extras that we can include or even quote to include are:

- Accidental Damage - meaning if something is accidentally damaged you have a potential claim

- All Risks - Insures your valuables away form the home (Rings/watches mobiles phones/Bikes etc)

- Home Emergency Cover - Gives access to tradespeople (Burst pipes/flooding/boiler breakdown)

- Legal Expenses - Provides you with FREE Access to legal advice for (Claims/Consumer issues/Land disputes/HR)

- Student Contents - when your children move out to University accommodation

- Replacement Keys - for lost or stolen keys

Landlords 'Rental Property' Insurance:

When you take a 'Buy to Let' Mortgage your lender will insist that you have landlord Insurance in place to protect your Building from the standard threats of storm, fire, flood etc .

- Landlord Insurance is slightly different to a residential household policy

- It will also include specific cover for all of the extra layers of legal responsibilities a landlord will have

- While similar to non rental property insurance, Landlords cover is even more essential due to the legal risks

- Optional Extras include: Rent Guarantee Cover/Malicious Damage Cover/Legal Expenses and Squatters Eviction

(Contact us for a quote and to explore all the options to suit your circumstances!)

Tips for dealing with your renewal:

In recent years, without exception, Home Insurance has all increased in cost each year at the renewal date.

Often, on paid via Direct Debit, means the cover will automatically renew. For this reason we recommend that you contact us 3-4 weeks BEFORE your renewal is due.

Why the price increases in recent years?

- Insurers payroll and premises costs have vastly increased

- Vastly increased reinstatement and repair costs

- The number of subsidence claims have increased (extreme weather patterns etc.)

- More instances of severe flooding claims (changing weather patterns)

- More (Named) Serious storms resulting in more large claims

Ways to make your home insurance cheaper?

Customers will always ask, how can we reduce the costs of their renewal:

- Consider moving provider - if you can obtain 'like for like' with another provider

- Take a higher excess (the amount you pay/deducted from your claim)

- Remove some of your extras (EG do you still want Accidental Damage?)

- Consider paying annually (paying monthly usually costs more)

- Check you are claiming all the possible discounts (Locks/Alarm etc)

- Finally, haggle with your Broker!

Documents we need to arrange your Mortgage

The list of documents we will need:

Typically, the initial documents we need to provide you with mortgage advice include:

- 3 months Pay Slips (13 payslips if paid weekly)

- P60

- Photo ID (Passport OR Driving Licence)

- last three months Bank Statements (PDF's & NOT Print outs)

- Most recent 'Annual Mortgage Statement' for any existing Mortgages (If you have had a mortgage)

- Copy of your Credit Report (Use the link on on website to obtain this)

- 5 Year address history

- Credit Report (See link below re: obtaining this)

- If Self Employed - last three years Tax Returns & last three years Tax Year Overviews

**When sending documents please make sure your send the complete PDF documents**

(In the process of gathering these, if you have any queries, call Alastair on 07710 66 95 42).

Warnings & Compliance Statements

*YOUR HOME IS AT RISK IF YOU FAIL TO KEEP UP REPAYMENTS ON A MORTGAGE

OR ANY LOAN SECURED ON THE PROPERTY*

*A PROTECTION PLAN WILL HAVE NO CASH VALUE AT ANY TIME & WILL CEASE AT THE END OF THE TERM*

WE ARE A CREDIT BROKER NOT A LENDER.

ACCESS FINANCIAL SERVICES LTD TYPICALLY RECEIVE COMMISSION FROM THE LENDER OR PROVIDER

FOR THE ARRANGEMENT OF YOUR MORTGAGE, FINANCE OR LIFE INSURANCE OR OTHER PROTECTION. THIS AMOUNT OF PAYMENT ACCESS FINANCIAL SERVICES RECIEVE WILL BE DISCLOSED ON RECEIPT OF

THE LENDER’S OR PROVIDER’S OFFER OR ILLUSTRATION.

(DIFFERENT LENDERS OR PROVIDERS WORK WITH DIFFERENT COMMISSION MODELS)

*********

- ‘Fermanagh Mortgages’ is a Trading Style of Access Financial Services Limited.

- We will receive commission from lenders. Different lenders pay different amounts depending on different commission models. For transparency we work with the following commission models: percentage of the amount you borrow. Further details of the commission model, calculation and amount will be disclosed to you throughout your customer journey.

- We work with an unrestricted number of Lenders to find a potentially suitable product.

- Access financial Services ICO Registration No. is Z564037X, and Fermanagh Mortgages ICO Registration number: ZB551481.

- The Financial Conduct Authority do not regulate Bridging/Commercial loans and certain types of Buy to Let Mortgage and some investment mortgage contracts. Equity Release/Home Reversion (For the Lifetime Mortgage/Home Reversion Plan, we will provide you with a personalised illustration, so that you understand the risks and complex features of such mortgages).

- Under no circumstances should any of the information contained within this website be construed as "advice". You should seek professional advice in respect of your own circumstances

- Access Financial Services Limited is authorised & regulated by the Financial Conduct Authority; the Financial Services Register number is 301173. Access Financial Services Limited is a Company registered in England & Wales, registration number 04427489 whose Registered office is Unit 1, Furtho Court, Towcester Rd, Old Stratford, Milton Keynes, MK19 6AN (please use the links on our website above to see full details of our Terms of Business & all other IMPORTANT documents)

- All income receivable is paid to 'Access Financial Services Limited' directly, with a proportion of this, then being paid to your 'Fermanagh Mortgages' Adviser.